Our team is committed to continuing to serve all your real estate needs while incorporating safety protocol to protect all of our loved ones.

In addition, as your local real estate experts, we feel it’s our duty to give you, our valued client, all the information you need to better understand our local real estate market. Whether you’re buying or selling, we want to make sure you have the best, most pertinent information, so we’ve put together this monthly analysis breaking down specifics about the market.

As we all navigate this together, please don’t hesitate to reach out to us with any questions or concerns. We’re here to support you.

– Vivian Yoon & Dennis Hsii , DRE #01925833 / DRE #01919746

Welcome to our July newsletter, where we’ll explore residential real estate trends in the North Beach, West Side, and South Bay markets in Los Angeles and across the nation. This month, we examine how buyer demand might shift during the rest of the year, taking into account the historically low inventory, record high prices, and the Federal Reserve Bank’s incentives to keep interest rates low despite rising inflation.

We’ve entered into an economic situation that is uncommon, at least in recent history, with rising inflation and high unemployment. The Federal Reserve Bank (the Fed) has two goals known as the dual mandate: price stability (inflation) and maximum sustainable employment. The pandemic, of course, threw a sizable wrench in the economic machine, causing mass unemployment from which we are still recovering. Easy monetary policy brought more money into circulation and a drop in interest rates.

The low-rate environment spurred homebuying across the country, lowering available inventory and driving home prices to record highs. Most potential buyers are flush with cash and have high credit scores, which has created an incredibly competitive environment. How will the massive price increases we’ve seen over the last year affect demand? And how will the market respond to a price correction?

As we navigate this period of high buyer demand and low supply, we remain committed to providing you with the most current market information so that you feel supported and informed in your buying and selling decisions. In this month’s newsletter, we cover the following:

Key Topics and Trends in July: The Fed will continue to keep rates low through 2021, which will continue driving the demand for homes. Despite high demand, low inventory and climbing home prices will price some potential buyers out of the market.

July Housing Market Updates for selected Los Angeles areas: Single-family home inventory has returned to pre-pandemic levels and demand in the areas is high, driving prices in the North Beach and the West Side to their highest levels in two years.

Key Topics and Trends in July

The past year saw the highest sales volume and fastest price increases on record nationally. We want to take a closer look at this massive buyer demand, and the ways in which it’s affecting the housing market.

At the start of the pandemic, the housing market looked incredibly unstable: buyers and sellers were pulling out of deals, sales volume and inventory dropped, and unemployment skyrocketed. The uncertainty around the housing market was short-lived, however, and it became clear that homes were going to have a remarkable year.

The Fed’s easy monetary policy over the last year has caused a swift rise in inflation, about 5%. After a decade of relatively low inflation, often under 2% annually, consumers are noticing the price jumps. In fact, there was slightly more inflation during the year from May 2020 to May 2021 than there was during the three-year period from 2017 to 2020. The price increases are partly due to monetary policy and partly due to global supply chain disruptions caused by the pandemic. As the pandemic fades on a more global basis and supply chains stabilize, prices should correct, at least to an extent. For the moment, the Fed has decided to keep interest rates low and continue infusing money into the economy.

Even though inflation has become more noticeable, the Fed still must consider the employment rate. As you can see from the chart below, employment hasn’t reached pre-pandemic levels, and the growth rate has slowed. Because employment typically grows at such a constant rate, we still have around 10.5 million fewer employed people than if there had never been a pandemic.

The Case-Shiller 20-City Home Price Index, which measures the aggregate home prices in the 20 largest metro areas, rose 15% year-over-year in April 2021, marking one of the sharpest increases in history. The Fed also has incentives to prevent the housing market from crashing. A sharp drop in home prices would wipe out significant wealth and put many new homeowners underwater. These are huge disincentives to change the current path.

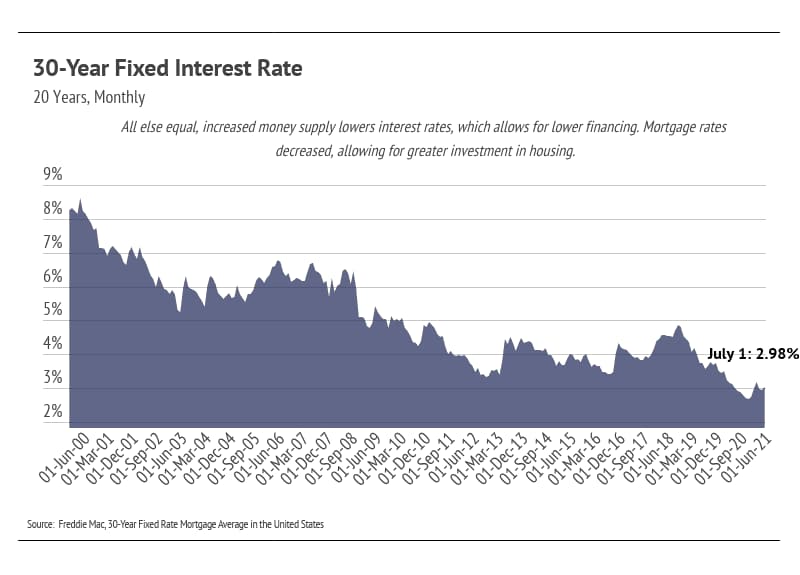

As shown in the chart below, we’re currently hovering at historically low mortgage rates, which will likely remain for the rest of the year. As mentioned earlier, low rates incentivize buying, as does inflation. When consumers know the dollar’s purchasing power is diminishing more quickly, then buying a home sooner rather than later makes more sense.

In 2020, incentives to purchase a home have translated to the most homes sold in a year since 2006. Although we’re only halfway through 2021, it’s safe to say that home sales will outpace those in 2020.

As we look at the last 12 months of annualized home sales in the chart below, we see sales slowing. This is largely caused by the lack of inventory. There are simply not enough homes to meet the current demand. Even if some potential buyers get priced out, the housing market will not see much of a change.

The environment, therefore, is right for demand to outpace supply in 2021. We’ve reached near-perfect conditions for qualified buyers—high credit scores, large down payments, and low-rate financing—so we anticipate a competitive landscape for buyers throughout the year.

While the market remains competitive for buyers, conditions are making it an exceptional time for homeowners to sell. Low inventory means sellers will receive multiple offers with fewer concessions. Because sellers are often selling one home and buying another, it’s essential that sellers work with the right agent to ensure the transition goes smoothly.

July Housing Market Updates for selected

Los Angeles areas

In this newsletter, we break down three luxury areas in Los Angeles as follows:

North Beach: includes the Pacific Palisades, Santa Monica, and Venice

West Side: includes Beverly Hills, Brentwood, West Hollywood, and Westwood

South Bay: includes Hermosa, Manhattan Beach, and Redondo

During June 2021, median single-family home prices rose month-over-month in North Beach and the West Side. The median home price in the South Bay declined slightly off the May peak. Year-over-year, single-family home prices increased in North Beach and the West Side, while the South Bay was flat.

Single-family home inventory grew much higher for North Beach and the West Side in 2020 relative to 2019, while the South Bay trended similarly to 2019 (a “normal” year) in 2020. The unusual spike in inventory was short-lived due to demand in the area. In the selected markets, inventory retracted as quickly as it increased and is now trending similarly to pre-pandemic levels. Since the start of 2021, more new listings have been coming to market, but these were met with increased sales. Demand in the area is significantly higher than last year and will likely absorb many of the new listings that come to market this summer. The sustained low inventory will likely cause prices to appreciate throughout 2021.

Days on Market have declined substantially since the start of 2021. Homes are still selling relatively quickly for luxury markets. As we’ll see, the pace of sales has contributed to the low Months of Supply Inventory (MSI) over the past several months.

We can use Months of Supply Inventory (MSI) as a metric to judge whether the market favors buyers or sellers. The average MSI is three months in California (far lower than the national average of six months), which indicates a balanced market. An MSI lower than three means that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI means there are more sellers than buyers (meaning it’s a buyers’ market). In June 2021, the MSI remained below three in the South Bay, highlighting the demand in the area. North Beach is balanced with 3.3 months of supply, and the West Side MSI favors buyers with 4.5 months of supply.

In summary, the high demand and low supply present in the selected Los Angeles areas have driven home prices up. Inventory will likely remain low this year with the sustained high demand in the area. Overall, the housing market has shown its value through the pandemic and remains one of the most valuable asset classes. The data show that housing has remained consistently strong throughout this period.

We expect that the number of new listings will increase in the summer months. The current market conditions, however, can withstand a high number of new listings coming to market, and more sellers may also enter the market to capitalize on the high buyer demand. As we navigate the summer season, we expect the high demand to continue, and new houses on the market to be sold quickly.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we have shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.